If you’re self-employed and looking to get the most out of KiwiSaver, this article will assist you by providing general contribution instructions and some tips on maximising your balance by utilising the initiatives KiwiSaver has on offer.

Self-employment gives you the ability to choose your own hours, decide on which projects or jobs you undertake and can often lead to a higher than market take-home pay, but self-employed Kiwi’s frequently take an unexpected financial hit…

Being self-employed can lead to a lower KiwiSaver balance for use as your first-home deposit or for retirement. This is because it’s not mandatory for you to contribute a percentage of your wage to your KiwiSaver account, plus there’s no employer to match your contributions (unless your own company is matching your contributions). Sure, in the short term you see more money in your bank account, however the long-term negatives are not jumping on the property ladder as fast and reaching or nearing retirement with a significantly below-average nest egg. Who wants to work through their golden years?

Here’s how to ensure you make the most out of KiwiSaver, while still reaping the benefits of self-employment.

How to deposit money into your KiwiSaver account if you’re self-employed

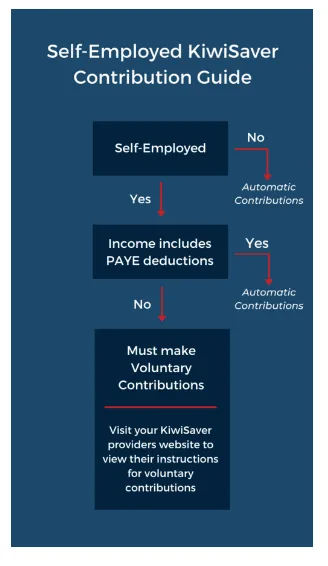

If you are self-employed and your income includes PAYE deductions, then KiwiSaver contributions will automatically be deducted from your gross pay at a minimum of 3.5% (with 3.5% matched).

So for example if you work through a recruiter, and you receive payment from that system, then your income is likely coming with PAYE deductions. You can find more information on PAYE deductions here.

If you’re self-employed and your income is not subject to PAYE deductions, then you will have to make voluntary contributions directly into your KiwiSaver account.

An employment style that would fall under this situation would be a freelancer, who bills clients directly.

To make the voluntary contributions, your KiwiSaver provider will have instructions on how to make one-off contributions, or how to set up an automatic payment to contribute.

Regularly contributing a set amount ensures that you take full advantage of dollar-cost averaging. Even if you are only looking to contribute enough to maximise the annual Government contributions, then setting up an auto-payment may still be a great option as it won’t feel like such an outgoing. An auto-payment of $21/week, $41/fortnight, or $87/month is enough to make sure that you receive the full $260.72 Government contribution each year.

If you need a hand with depositing money into your KiwiSaver account or just some general guidance, then please get in touch via the button below, and we can get an adviser to review your situation free of charge.

Maximising Government Contributions while Self-Employed

The first tip is to take advantage of the annual Government contribution each year. A guaranteed 50% return on your investment is a good deal no matter where it comes from.

If you’re an eligible KiwiSaver member, you will receive $0.25 for every $1.00 that you contribute towards KiwiSaver up to a maximum of $260.72 every year. To receive the maximum amount, you must contribute $1,042.86 annually. The KiwiSaver year begins on the 1st of July and ends on the 30th of June, so make sure you contribute $1,042.86 in this window.

Take a look at the following criteria to make sure that you’re eligible…

- You must be over the age of 16 and under the age of 65

- You must be typically residing in New Zealand

- You must be a KiwiSaver member prior to the start of the KiwiSaver Government contribution year to receive the maximum government contribution. If you became a KiwiSaver member during the year, you are entitled to a prorated contribution (i.e. if you joined on 1 October, or 3 months through the year, you would be eligible to receive 75% of the Government contribution)

Contributing a set amount of your income

The next tip on using KiwiSaver when you’re self-employed is to regularly contribute a set amount of your income towards your KiwiSaver account. This might seem like pretty general advice, but there’s something larger at play here.

KiwiSaver investors grow their balances so rapidly because they invest when the markets are performing well… and not so well. This is an investment strategy known as dollar-cost averaging.

There’s plenty of articles explaining the ins and outs of dollar-cost averaging and why it generates such great returns, however it can be boiled down to this; continually buying when the market experiences dips, and then holding for when the market rallies again.

It’s no secret that this investment strategy works, and it’s the main reason every country in the OECD (with exception to New Zealand and Ireland) has a mandatory retirement savings scheme. If you’re self-employed, make the most of this investment strategy and consider contributing at least 7% of your before tax income towards KiwiSaver like non-self-employed workers.

Do note that if you’re self-employed and you do not receive PAYE income (for example a contractor who invoices for contract work), you do not need to match any KiwiSaver contributions made. If you are self-employed and the income which you pay yourself incurs PAYE deductions, you will be considered an employee for KiwiSaver purposes and as you are also the employer you will have to match your employee contributions up to a minimum of 3.5%.

Looking for some more KiwiSaver guidance?

At Invested Partners Limited, we advise self-employed Kiwi’s free of charge on how to maximise their KiwiSaver savings. If you’d like to talk with me and get your KiwiSaver account on track, just click here.

Get A KiwiSaver Recommendation

Photo by Maranda Vandergriff on Unsplash