Dollar cost averaging is an important investment strategy that can occur organically with KiwiSaver. In this article we discuss how New Zealanders can benefit from this strategy, ensuring their KiwiSaver balance is protected during downfalls in the market, and taking full advantage of upward swings.

When markets are tumbling, it’s human nature to steer clear of investing and sit on the sidelines. Worse yet, many people get cold feet and either sell their investments or switch their investments from a growth approach to a more conservative approach. This is a completely natural thought process; however it can be one of the biggest mistakes when it comes to investing.

What Is Dollar Cost Averaging?

Dollar cost averaging is the strategy of investing a consistent amount on a regular basis. This is a very simple method, however it is much more difficult to execute in practice due to the natural instinct of not wanting to invest when the prices of investments are decreasing.

How Does Dollar Cost Averaging Relate To KiwiSaver?

You have likely implemented the dollar cost averaging investment strategy just by being part of the KiwiSaver scheme. For anyone that earns PAYE income (i.e. employed by a company), you and your employer are contributing a set amount towards your KiwiSaver on a regular basis. People who have set up direct debits for their KiwiSaver are also taking advantage of dollar cost averaging as they’re also contributing a set amount on a regular basis towards their investment.

What Is The Benefit Of Dollar Cost Averaging In Relation To Your KiwiSaver Investment?

The benefit of dollar cost averaging is that you buy less units when the prices are higher (i.e. when markets are performing well) and more units when prices are lower*. It’s similar to putting $50 of gas in your car, when the price of fuel is higher you get fewer litres of fuel, however when the price is lower that same $50 buys you more litres.

*your KiwiSaver balance is calculated as units of the underlying KiwiSaver fund owned x unit price (i.e. 10,000 units x $3.50 = $35,000 KiwiSaver balance)

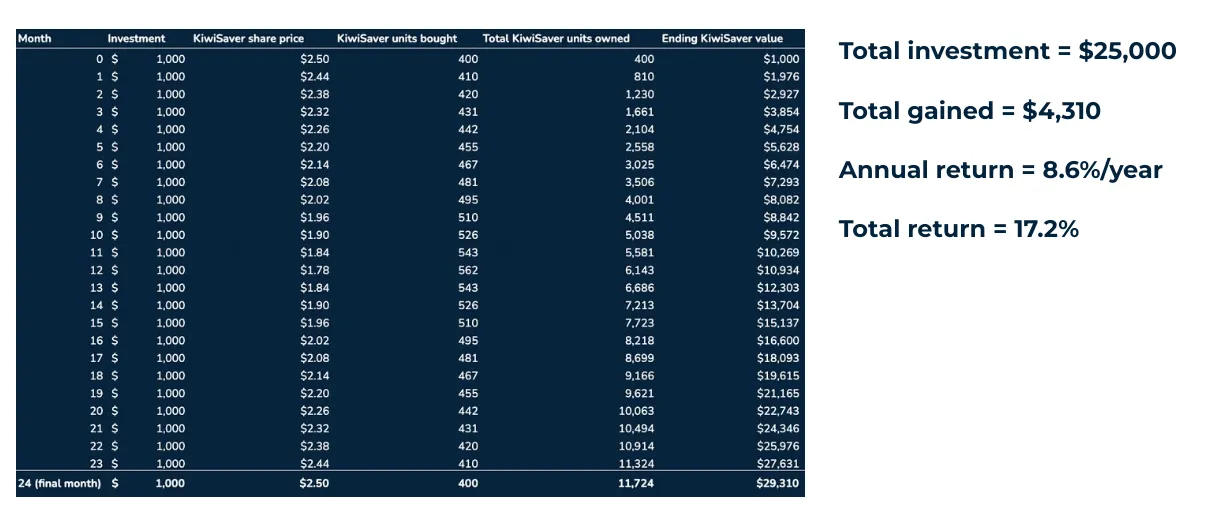

Dollar Cost Averaging In Action

So now that you know that you’re buying more units of your KiwiSaver fund when the price is low, or when markets are falling, how does this benefit you in dollar terms?

In this example, our KiwiSaver client decides to contribute $1,000 a month into their fund. Right from the beginning, the market crashes and their fund drops by 29% over the next 12 months. Our KiwiSaver client is feeling disheartened with their decision, however sticks to their fund and strategy. Things then brighten up, and the market recovers over the next 12 months, bringing the unit price of their fund back to its original price. Their fund returned 0% over this 2 year period, however our KiwiSaver investor still made money as shown below…

Although our example’s KiwiSaver fund was priced at $2.50/unit at the beginning, and $2.50/unit at the end, therefore a 0% movement overall, they still came away with generating 17.2% over the 2 years. They generated this return simply by regularly contributing, therefore buying more units when the price dropped, and less when it increased again. This is the magic of dollar cost averaging, and it can’t be ignored when making investment decisions in relation to KiwiSaver.

When Does Dollar Cost Averaging Not Work?

Dollar cost averaging won’t work when what you’re investing in is a poor investment which won’t recover in the long term. This is certainly a possibility when it comes to non-diversified or inherently risky investments.

Dollar cost averaging also won’t work if you don’t have enough time to let the markets recover.

In saying this, if you have received a KiwiSaver recommendation from us, your KiwiSaver account is diversified by being invested across a range of geographies, industries and asset types, therefore acting more like an investment in the market rather than a single asset (stock). The market increases over the long term and has always recovered from any drawbacks it’s experienced. Therefore, over the long term we deem it as a relatively safe investment.

Furthermore, if you’ve received a recommendation from us, we have put you in a fund that aligns with your investment horizon so you either; have enough time for the markets to recover, you’re in a fund that isn’t susceptible to market volatility, or you’re invested somewhere in between.

Is Your KiwiSaver Investment Optimised For You?

If you want to ensure that your KiwiSaver account is appropriately diversified, and that it’s aligned with your investment horizon and goals, please fill out our Fact Find by clicking on the link below so that you can receive a free KiwiSaver recommendation. Make sure to act on it!